How to Prevent Credit Card Chargebacks: 7 Tips You Can Use

Across all industries, the average credit card chargeback rate is 0.60 percent. That’s perilously close to the danger zone of 1 percent, at which point the company will be on the credit card industry’s MATCH (Member Alert to Control High-Risk Merchants) list. That makes it very hard if not impossible for the company to secure merchant services.

Whether you’re not there yet or if you’ve been there and back, you know how important it is to prevent credit card chargebacks. Let’s attack the problem by looking at the different reasons why chargebacks happen and the ways you can prevent each one.

Friendly Fraud

Chargebacks exist because credit card companies wanted to protect consumers from fraudulent transactions. Unfortunately, some consumers have begun to take advantage of this law. It’s called friendly fraud, and it can be intentional or unintentional.

Unintentional friendly fraud happens when the customer knowingly makes a purchase but doesn’t recognize the charge on his or her bank statement. Clarity is the key to keeping these kinds of chargebacks off of your record.

Tip #1: Make sure your billing descriptor features your brand name.

Some brands – eCommerce as well as brick-and-mortar – use their parent company names rather than the brand name their customers will recognize, causing customers to dispute the charge. If you print the name of the store they actually bought from, they’re more likely to remember the transaction.

Tip #2: Include your customer service phone number too.

Many chargebacks happen when a customer simply forgets a purchase. Maybe your system charged the customer’s card after the item shipped, which happened days or even weeks after the original order. By the time he or she sees the line item, the purchase has been forgotten.

If you include a phone number in your billing descriptor, you give the customer a chance to call you and ask about the charge. You can offer a reminder and avoid an unnecessary chargeback.

Intentional friendly fraud is more insidious. It happens when the customer pays for and receives a purchase, but claims that it was fraudulent or unauthorized.

These chargebacks can be hard to fight because they’re hard to dispute, particularly in the case of eCommerce transactions. The merchant has the burden of proof that the transaction was legitimate, and it’s very hard to prove that an item didn’t get lost or damaged in shipping, or that someone wasn’t impersonating the buyer.

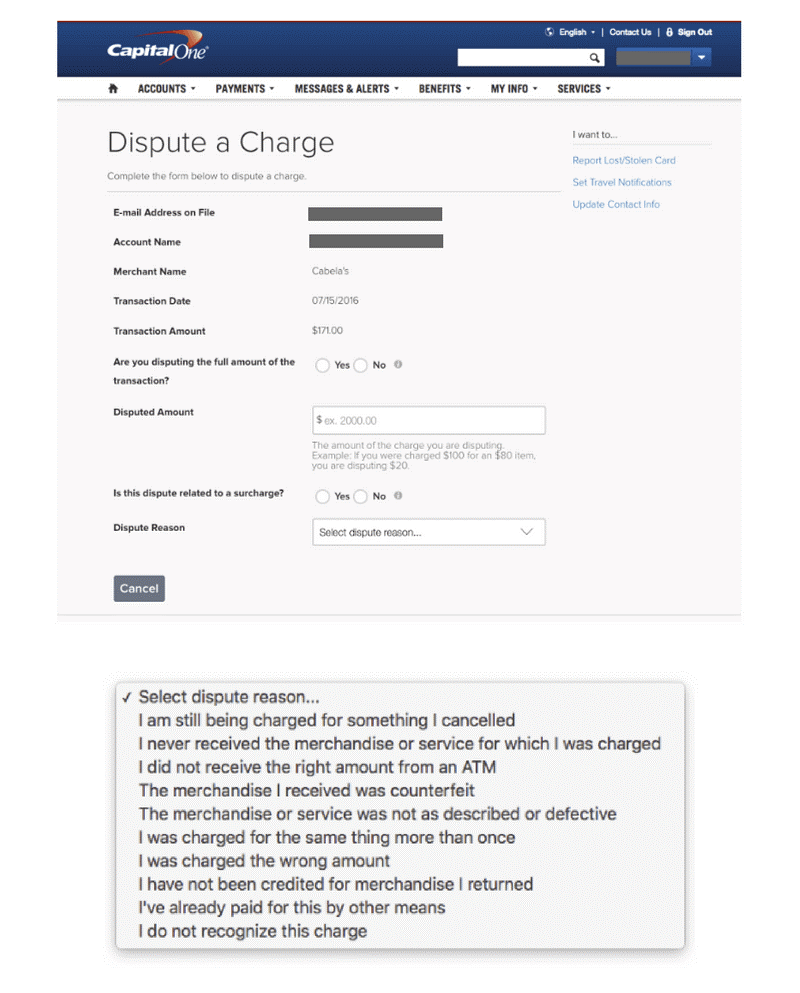

Tip #3: Dispute chargebacks that seem fishy.

Unless you’ve talked to the customer and figured out that there was an error, whether mechanical or human, take the time to dispute a chargeback. It’s the only way to get back the lost revenue and the chargeback fee.

It does take time to collect and present evidence to plead your case. And you may not always win. But if you don’t respond, you’re making it easy for people to defraud you. And if it’s easy, what’s to stop them from doing it again?

Tip #4: Keep thorough records, all the way to delivery.

To win a chargeback dispute, you have to produce “compelling evidence” that the transaction is valid and complete. The more data points you have on the transaction, the more convincing you’ll be.

If you have a physical store selling a physical product, you’re lucky. You probably have more documentation, including physical receipts or invoices. If you do business online, you might need to do more digging, but the proof is there:

- Copies of customer communications

- Address Verification Service (AVS) and Card Verification Value (CVV) match data

- Proof of product usage – social media photos, evidence of digital use, etc.

- Copies of emailed invoices

- Terms and conditions from the purchase transaction

The more you can present, the more effectively you can dispute chargebacks and the less appealing of a target you will be to fraudsters.

Criminal Fraud

This is the most famous kind of fraud. It involves stolen credit cards or credit card numbers. It is, as mentioned, the reason why chargebacks exist.

Criminal fraud is frustrating for card issuers because they did nothing wrong, yet they still lose the revenue from the fraudulent transaction. Chances are, they’ll never get the product or service agreement back either.

To prevent criminal fraud, you have to be very aware and very proactive about security.

Tip #5: Look out for signs of fraud during proof-of-sale.

Don’t get caught finding out the hard way how credit card fraudsters operate. Do some research and learn to spot the warning signs. For eCommerce, these include:

- A billing address that doesn’t match the IP address

- One IP address, multiple orders on different cards

- A failed AVS or CVV check

- Costly expedited shipping for a low-value order

During brick-and-mortar sales, watch out for:

- Customers with no forms of ID

- Damaged magnetic strips

- Letters from the “cardholder” authorizing borrowed use

This list is far from exhaustive, simply because there are as many fraud strategies as there are perpetrators. Always be on the lookout for a transaction that appears out of the ordinary; it’s better to be safe than sorry.

Tip #6: Use secure payment processing.

If your merchant services aren’t proactive about keeping customer data safe and preventing fraudulent transactions, find a new vendor. You want one that’s aligned with Payment Card Industry (PCI) Data Security Standards and that helps you to become compliant as well.

Don’t think it can’t happen to you – in 2015 alone, 73 percent of companies experienced payments fraud.

Merchant Error

Sometimes there really is something wrong with the product or order. Maybe it arrived broken or was a different color than the customer ordered. You can still prevent a chargeback!

Tip #7: Respond to customer complaints quickly and thoroughly.

If customers can’t get a refund through the company, they might try to file a chargeback instead. Head them off at the pass by responding to complaints quickly and working to resolve them to the customer’s satisfaction.

The Take-Away

You can’t prevent every chargeback, just like you can’t dispute every one you get successfully. But each one you can prevent is a chargeback fee saved and revenue retained. It’s worth your time to keep an eye on your credit card processing activity and see if you’re getting a lot of chargebacks of one kind or another. If you can stop it, your bottom line will thank you.

Get In Touch

Want to improve your payment experience?

Speak with a dedicated account manager today.

Popular

-

USA Epay

USA Epay

05 17, 2016 -

Processing Check Payments: Making the Most of Risk Management Resources

Processing Check Payments: Making the Most of Risk Management Resources

07 15, 2016 -

How Having a POS System Can Benefit Your Business

How Having a POS System Can Benefit Your Business

07 18, 2016 -

Success Tips for Entrepreneurs

Success Tips for Entrepreneurs

08 02, 2016

Ready to get started?

Get in touch or create an account